STORY UPDATED: check for updates below.

Does California give away interest-free home loans exclusively to "people who came into this country illegally," bypassing U.S. citizens? No, that's not true: California's AB-1840 bill never proposed such a measure. U.S. citizens who meet specific requirements are already eligible to participate in the California Dream for All program, and the 2024 bill would not change that.

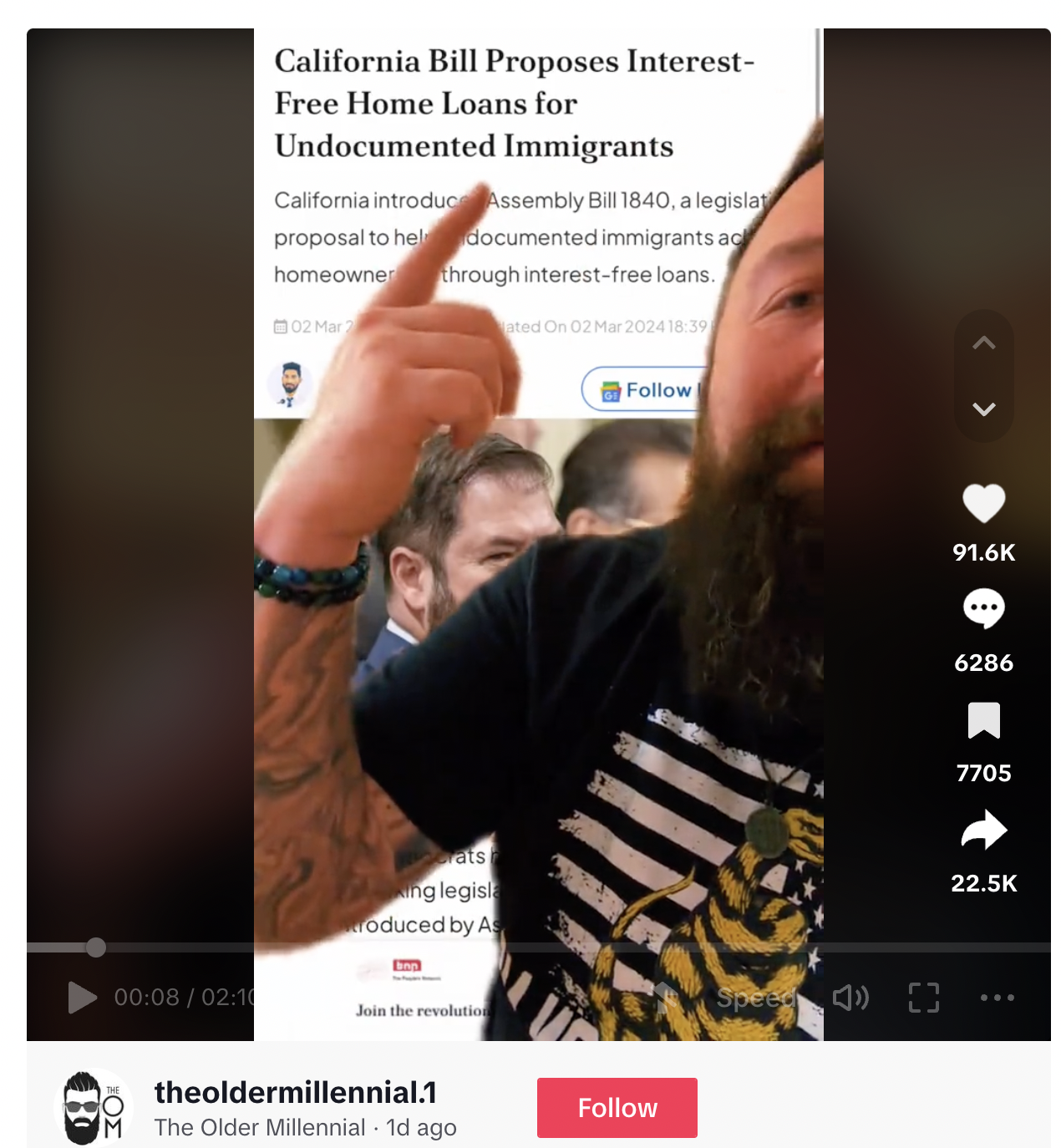

The claim appeared in a video (archived here) on TikTok on March 5, 2024. It showed a bearded man saying:

I think it's kind of cool that California is working on giving first-time homebuyers interest-free and payment-free loans for their home. AHA psych, motherfuckers! It's only for illegals!

He continued:

People who came into this country illegally, people that are not supposed to be here -- and they are giving it to them, instead of Californians!

This is what the post looked like on TikTok at the time of writing:

(Source: TikTok screenshot taken on Wed Mar 6 19:07:48 2024 UTC)

The claim, however, distorted the proposal.

An early version of the California bill AB-1840 (archived here) introduced on January 16, 2024, did mention "undocumented persons" but only as one of the potentially eligible categories. By the time the claim was published on TikTok, the legislation had already been amended to exclude that language. As of February 28, 2024, with strike-throughs added during the legislative process, it read (archived here):

This bill would specify that the definition of "first-time homebuyer" includes, but is not limited to, undocumented persons. an applicant under the program shall not be disqualified solely based on the applicant's immigration status.

Contrary to what the man in the video says, the bill has never aimed to establish a brand-new home-owning program designed exclusively for immigrants, documented or undocumented. The first paragraph of the legislative proposal sponsored by Assemblymember Joaquin Arambula (archived here) explicitly referred to an existing program, California Dream for All (archived here.)

His legislative director Jacob Moss confirmed that to Lead Stories via email on March 7, 2024:

There is nothing exclusive about the program to undocumented immigrants. The bill was always additive and clarifying. It didn't modify in any way how citizens are able to access the program or create any type of priority or preference for any applicant.

According to the program's website, it "offers up to 20% for down payment or closing costs, not to exceed $150,000" for first-time homebuyers whose household income is not greater than specific amounts and one of whom has to be also a first-generation homebuyer (the State of California distinguishes between the two).

The existing program's handbook, last updated in January 2024, explicitly mentions U.S. citizens in the eligibility section as well as "qualified aliens" as defined at 8 U.S.C § 1641 (archived here). This section of the U.S. Code describes people who are either legal permanent residents or fall under very specific exceptions under the U.S. law.

In reality, however, the pool of noncitizens who can benefit from the program is much smaller. Besides green card holders, it is mostly limited to DACA recipients, Moss told Lead Stories:

The 'qualified aliens' in this program are only those able to get a mortgage loan. This means folks who are able to get an ITIN, which will almost always be DACA folks. There is no scenario that an undocumented person without a SSN or ITIN will be able to get a bank loan which means there is no scenario that they would qualify for a Dream for All investment. ... We just want to ensure that if a bank is willing to lend, the state doesn't have a more stringent standard that inadvertently excludes people when inclusion of these people has been the stated goal of the program all along.

As Lead Stories previously wrote, DACA recipients are not "illegally" in this country.

While financial institutions are not supposed to discriminate based on an applicant's immigration status and deny loans to otherwise eligible people, they are allowed to consider (archived here) it "when necessary to ascertain the creditor's rights regarding repayment." And the line between overreliance on this indicator and reasonable consideration does not appear to be clearly defined.

Other Lead Stories fact checks mentioning immigration can be found here.

Updates:

-

2024-03-08T00:30:41Z 2024-03-08T00:30:41Z Adds quotes from the legislative director for Assemblymember Joaquin Arambula.